My 2¢s and 5 Big Takeaways

Okay, before you start using your AI detection tools, I want to provide a summary of the report from Perplexity. I have five key takeaways from the report (yes, I wrote these).

- The Grid Better Get Ready - When you see power companies that are very conservative start to build prototype plants, it would seem a fair indication that we have seen more than the general public has, and we are closer than we think. As a fan of the Summer Olympics and World Cup, four years go by faster than it seems, and the timeline to fusion seems much closer than I believe many appreciate.

- Money Talks - The money continues to flow toward fusion, new sites, and construction. I know some folks who say these are billionaires who don’t understand the science and are using “play money.” I would say these folks did not achieve their success and stations in life by being fooled very often. If Gates, Bezos, Altman, Zuckerberg, and the others of the billionaire class are all wrong about fusion, I would be very surprised.

- I Still Believe in People - Today marks my second anniversary at Peak Nano, where I work in the fusion space. The people I have met are smart, capable, and clear-eyed about the challenges, yet they believe they can overcome those challenges. Ultimately, it is people of passion, conviction, and perseverance who change the world, while others are merely detractors on the sidelines. I will bet with these fusion people versus the naysayers.

- China is Chasing Victory - China can do almost anything it wants from an R&D and supply chain perspective, and it is betting big (2-3X more than the US) in funds, lands, and people to make fusion happen. These are smart and motivated people who envision a fusion future, and their actions suggest they believe they are right about fusion energy, so we should keep up.

- The Timeline is not Slipshod - Now I realize that we are asking people who believe in and have a vested interest in fusion if fusion is going to happen and when. However, the timelines are not slipping year over year in these surveys. That tells me these folks are closer than the skeptics want to believe.

Enjoy the summary, download the report, and thank Andrew Holland, Caroline Anderson, the FIA team, and the vendors who made this report possible.

The 2025 Global Fusion Industry Report (with help from Perplexity)

In 2025, the fusion energy industry sits at a pivotal moment. What was once a field confined to academic laboratories and governmental research programs is now rapidly evolving into a commercially driven, globally competitive energy sector. According to the 2025 Global Fusion Industry Report by the Fusion Industry Association (FIA), fusion no longer seems like a technology perpetually 20 years away—it is an energy solution actively being engineered, tested, and piloted for commercialization in this decade.

The report, a result of collaboration from 53 companies across more than a dozen countries, provides a comprehensive view of the investments, breakthroughs, timelines, and challenges shaping this emerging industry. This global collaboration is a testament to the shared goal of delivering clean, safe, and virtually limitless electricity powered by nuclear fusion, making you a part of a larger movement.

Explosive Growth in Funding and Participation

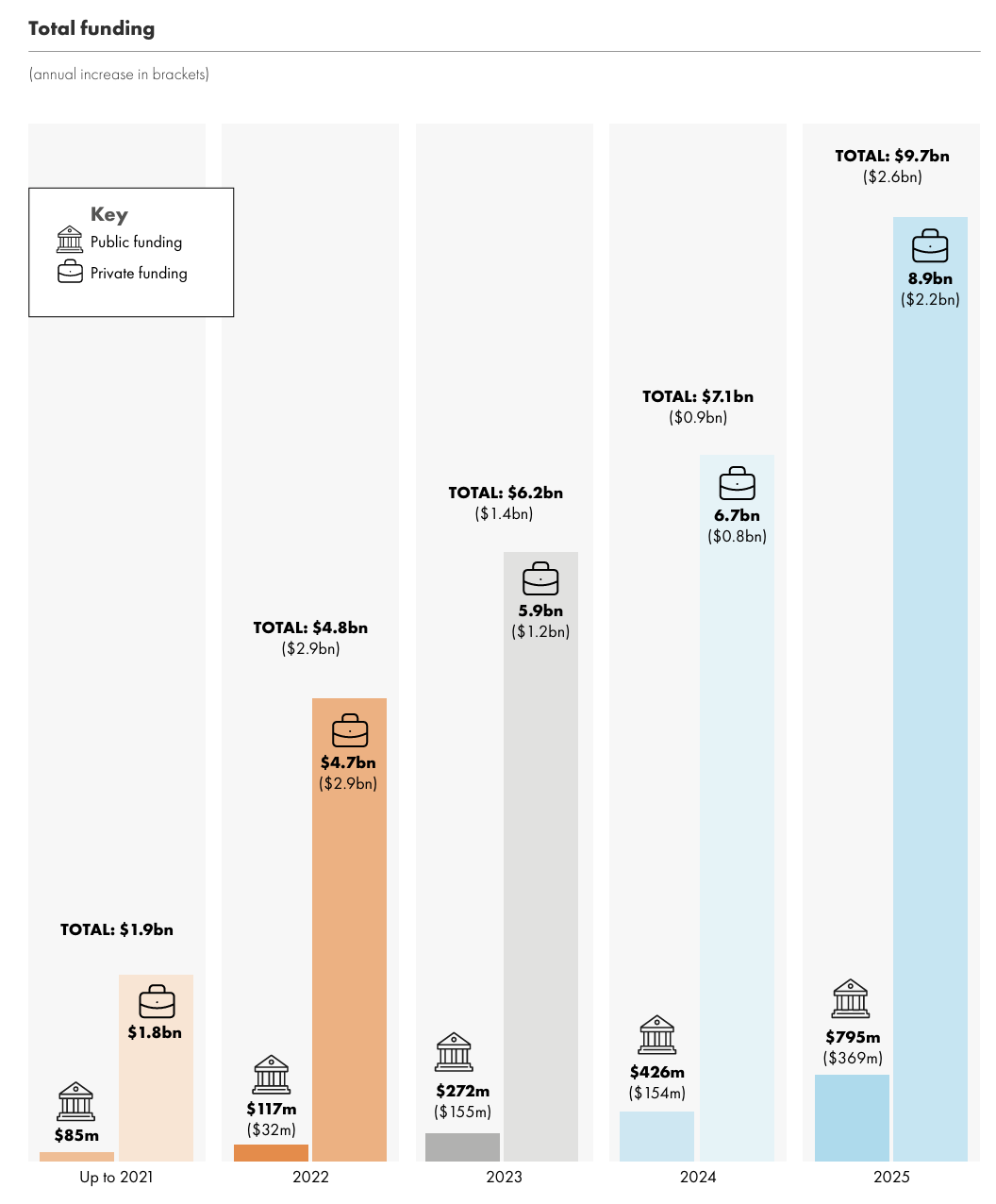

One of the most striking indicators of the industry’s maturation is the rapid escalation in funding. In 2021, private fusion companies reported a total of $1.9 billion in investments. By 2025, that figure has grown more than fivefold to $9.7 billion, with over $2.6 billion raised in the last year alone. The majority—roughly $8.9 billion—comes from private sources, but public funding has also increased, up 84% from the previous year to nearly $800 million1.

Governments across the globe—including the U.S., Japan, Germany, China, the U.K., and the EU—are not just watching from the sidelines. They are actively creating policy and entering into Public-Private Partnerships (PPPs) that share risk and accelerate commercialization. From DOE’s milestone-based fusion programs in the U.S. to siting support in Germany and the U.K., collaboration is increasing in both scale and frequency.

Parallel to funding, the company count and workforce have also expanded significantly, more than doubling in company number and quadrupling in headcount since 2021. The sector now directly employs over 4,600 people, and its broader supply chain supports at least 9,300 jobs, with projections reaching 18,200 employees when pilot plants are fully operational.

Fusion's Target Market and Commercial Momentum

While electricity generation remains the primary mission of nearly every fusion company surveyed, the emergence of secondary applications, such as industrial heat, off-grid energy, space propulsion, and medical isotopes, is a testament to the diverse and exciting potential of fusion energy. This should leave you feeling excited about the myriad ways fusion can revolutionize various industries.

Perhaps the most tangible sign of commercial viability is the emergence of Power Purchase Agreements (PPAs). In 2023, Helion Energy signed a landmark PPA with Microsoft for at least 50 MWe, with a similar agreement following with Nucor, the U.S.’s largest steel manufacturer. More recently, Commonwealth Fusion Systems (CFS)—the most heavily funded company at $2 billion+—signed a PPA with Google and announced its first plant near Richmond, Virginia, in collaboration with Dominion Energy1.

Site selection for initial fusion plants is well underway:

- Helion: Washington state

- Type One Energy: A retired coal plant in Tennessee.

- CFS: Chesterfield County, Virginia

- Focused Energy: Biblis, Germany

Fusion "hubs" are emerging in regions such as California, the Pacific Northwest, and the U.K.’s Oxford corridor, driven by both public support and private initiatives.

Who Are the Major Players?

Among the 53 companies surveyed, many are pushing the boundaries not just of physics but also of business models, partnerships, and R&D. Noteworthy players include:

- Commonwealth Fusion Systems (CFS): Backed by Google and MIT, using tokamak tech, aiming for ~$400 MWe output.

- Helion Energy: Using Field Reversed Configuration, the only firm deploying D-He3, with early deployment targeted for 2028.

- TAE Technologies: The longest-running private fusion firm, with over $1.3 billion raised, pursuing pB11 via beam-driven FRC.

- General Fusion: Based in Canada and focused on magnetized target fusion, currently testing the primary demo machine (LM26).

- Focused Energy: Germany-based laser fusion innovator, with designs for a 1.5 GWe plant and progress on components and R&D hubs.

The diversity of technical approaches is central to the industry's robustness. Magnetic confinement (tokamaks and stellarators) remains the dominant approach, used by 25 of the 53 companies, but laser inertial, magneto-inertial, hybrid electrostatic, and even muon-catalyzed fusion approaches are also being explored.

Timing: When Will Fusion Power the Grid?

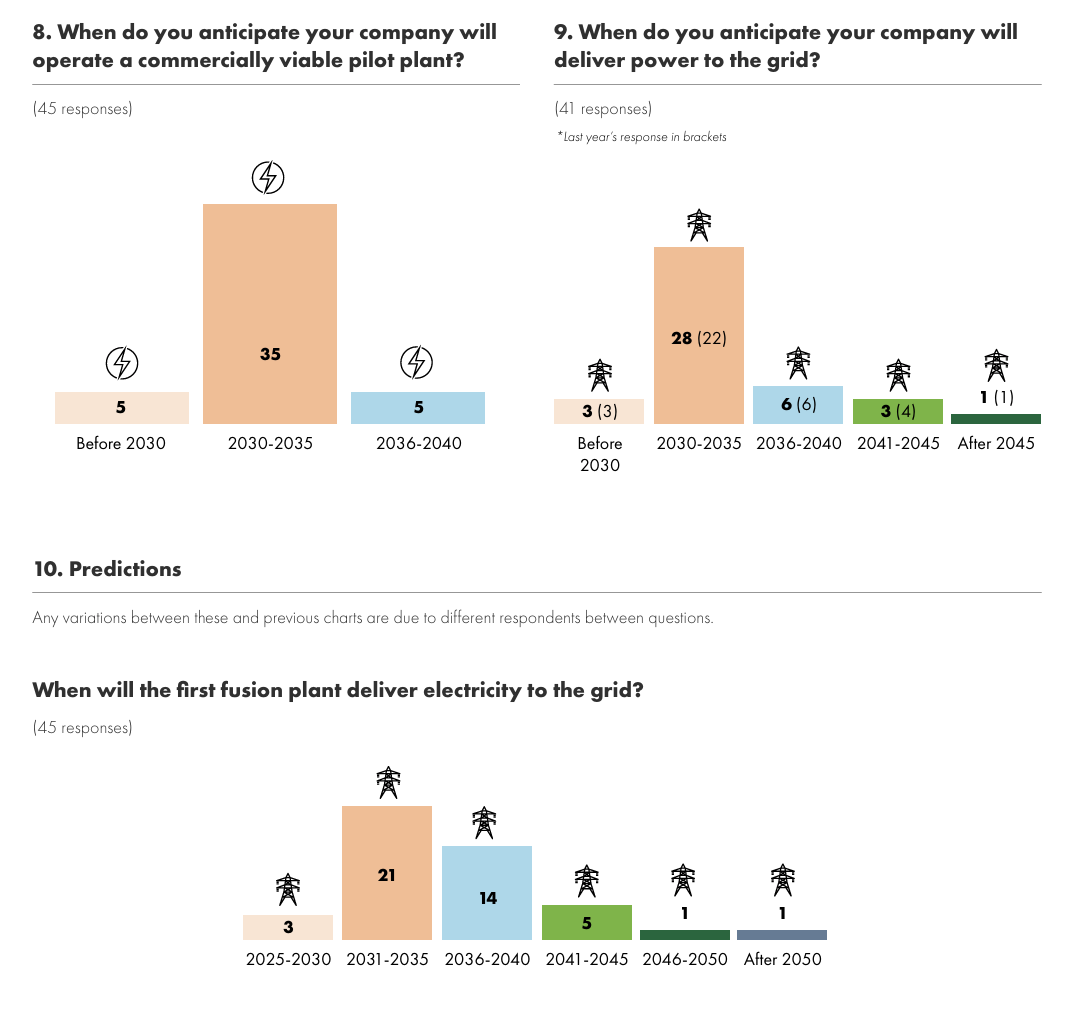

The industry is converging on the early 2030s as the decade of transformation. According to company forecasts:

- 35 out of 45 companies anticipate operating commercially viable pilot plants between 2030 and 2035.

- Twenty-eight companies expect to connect to the electric grid during the same period.

- Only five companies aim for commercialization before 2030, and few push timelines beyond 20401.

These pilot plants will demonstrate not only net energy (high-Q) operation but also the cost-effectiveness, cycle durability, and operational uptime necessary to deploy full-scale commercial reactors.

Challenges on the Road to Commercialization

Despite optimism, fusion developers face a dense thicket of hurdles:

Pre-2030 Challenges:

- Achieving sufficient fusion gain (Q > 1)

- Engineering neutron-resilient materials

- Developing fully integrated systems

- Ensuring tritium fuel cycle sufficiency

- Finding large-scale funding (median capital need: $700 million per company) to reach pilot plant stage 1

Post-2030 Concerns:

- Licensing and regulatory approvals

- Full lifecycle sustainability (waste management, decommissioning)

- Plasma exhaust and pulse duration issues

- Cryogenic systems and heat extraction

- Navigating geopolitical uncertainty and supply logistics1

Investment: A Broader and Deeper Pool

Fusion is attracting one of the most diverse sets of investors in the energy industry. On top of deep tech VCs like Breakthrough Energy Ventures and DCVC, the investor pool includes:

- Industrial giants: Chevron, Siemens Energy, Nucor

- Energy strategics: Shell Ventures, Energy Impact Partners

- Sovereign/quasi-public funds: In-Q-Tel, European Innovation Council

- Private tech founders: Sam Altman

- Telecom, real estate, defense sectors: Deutsche Telekom, Climentum, Special Invest1

This reflects a growing belief that fusion is not only technically viable but inevitable, and its applications will go far beyond traditional power grids.

Technological Spin-Offs and Ecosystem Growth

Beyond power generation, fusion R&D is giving rise to high-tech spinoffs. Advances in superconducting magnets, lasers, materials science, and plasma diagnostics are creating cross-sector opportunities in:

- Wind turbines and maglev trains

- Medical isotope production

- Neutron imaging and materials testing

- Space propulsion and tunneling tech1

This mirrors the innovation halo seen in the space race, where even failed moonshot efforts yielded valuable components, materials, and software.

Outlook: A Defining Decade

The fusion sector is in transition from bold ambition to substantive deployment. More than $77 billion would be needed (in aggregate) to commercialize all participating firms’ first plants fully, highlighting the scale of capital intensity and the importance of strategic consolidation.

Not every company will survive. However, just as in aviation or the semiconductor industry, a few leaders will emerge, and their success will ripple across economies and international energy markets.

Most importantly, fusion’s arrival coincides with mounting pressure to decarbonize, electrify infrastructure, and secure baseload energy in a shifting geopolitical climate. With projected outputs ranging from 5 kWe to 1.5 GWe per plant, fusion is being engineered to serve both remote microgrids and national grids.

A Global, Competitive Race

The 2025 fusion industry is, above all, a global one. Developers are headquartered in North America, Europe, Asia, and Oceania. The U.S. and U.K. remain performance leaders, but China, Germany, Japan, and Canada are quickly gaining ground, offering sites, funding, and authority alignment to draw innovation within their borders.

- https://www.fusionindustryassociation.org/fusion-industry-reports/

- https://ppl-ai-file-upload.s3.amazonaws.com/web/direct-files/attachments/13944827/28583bd4-c9ea-49ef-89a2-79dc8b473c66/2025-Global-Fusion-Industry-Report.pdf.pdf